Having worked on fintech apps that both failed and scaled, I’ve seen that success comes from strong banking partnerships, trust-first infrastructure, and smart monetization timing, the same approach Zelle follows. At AppVerticals, we’ve helped founders redesign fintech products around these exact principles.

Zelle moves hundreds of billions annually while staying free for users, making it a powerful case study in modern fintech strategy. This guide breaks down how Zelle makes money and the key lessons founders and investors should apply, from institutional monetization and embedded finance to security-driven growth and scalable product design.

Key Takeaways | How Does Zelle Make Money

- Zelle generates revenue through institutional transaction fees paid by partner banks, not end users.

- The platform earns from payment infrastructure licensing and secure API integrations embedded into banking apps.

- Fraud prevention and risk management technology function as monetized infrastructure services for financial institutions.

- High transaction volume enables scalable, low-cost network economics that drive recurring institutional revenue.

- Zelle strengthens bank retention and digital engagement, creating indirect monetization value through ecosystem growth.

- According to AppVerticals’ fintech experience, infrastructure-first monetization models outperform user-fee strategies at scale.

Understanding Zelle’s Business Model | What Makes It Work?

Zelle isn’t simply a standalone fintech app. It’s a bank-backed payment network operated by Early Warning Services, a company owned by major U.S. banks including JPMorgan Chase, Bank of America, and Wells Fargo.

That structure changes everything about monetization. Instead of competing with banks, Zelle strengthens them, embedding payments directly into their apps and ecosystems.

Why Zelle’s Distribution Model Works (Product & Growth Impact)

Zelle’s deep integration with banks lets users pay directly from their accounts, cutting acquisition costs, building trust, and reducing friction.

| Zelle Distribution Advantage | What It Means in Practice | Fintech Problem It Solves |

|---|---|---|

| Integrated with thousands of U.S. financial institutions | Built into existing banking ecosystems from day one | Reduces customer acquisition costs |

| Embedded directly into banking apps | Users access payments without downloading a new app | Eliminates trust barriers |

| Connected to existing bank accounts | No need for external wallets or onboarding friction | Minimizes payment friction |

At AppVerticals, I’ve seen fintech adoption increase dramatically once payment functionality was integrated into existing financial ecosystems instead of relying solely on standalone apps.

As adoption accelerates, companies increasingly partner with experienced teams offering fintech app development services to build secure, bank-integrated payment ecosystems.

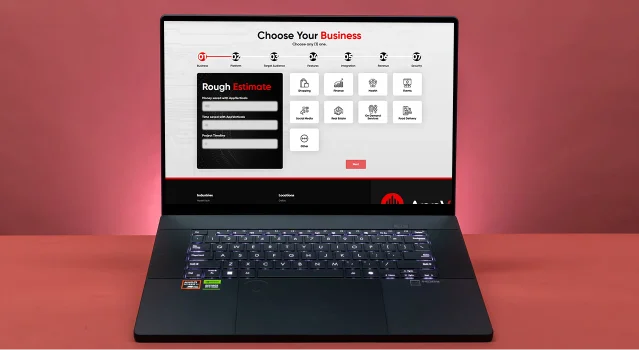

Revenue from Financial Institutions

So, how does Zelle make money? Zelle’s primary revenue streams come from:

- Transaction infrastructure fees paid by banks

- Payment network licensing

- Fraud prevention and risk management services

- Technology and API integration

Early Warning Services earns revenue by charging participating financial institutions small transaction-related fees rather than charging consumers directly.

Expert Insight:

“It is operated by Early Warning Services, a fintech co-owned by JPMorgan Chase (the nation’s largest bank), Bank of America, Capital One, PNC Bank, Truist, U.S. Bank, and Wells Fargo. Early Warning Services charges its thousands of financial institution partners a small fee for each Zelle transaction.”

This model aligns incentives with banks while keeping the product free for users, a critical growth strategy. With AppVerticals, you can also leverage these proven infrastructure-first strategies to build secure, bank-integrated fintech apps that scale without relying on user fees.

Build Your Own Bank-Integrated Fintech App

Turn your payment ideas into secure, scalable platforms like Zelle. Leverage AppVerticals’ expertise in mobile app development, real-time payment rails, and embedded finance.

Transaction Volume and Cost Efficiency

High transaction volume is the backbone of Zelle’s monetization. Zelle has processed hundreds of billions in annual payment volume, enabling:

- Low marginal transaction costs

- Scalable infrastructure economics

- Stable recurring institutional revenue

Promoting Cross-Selling and Customer Retention

Banks benefit from Zelle through:

- Increased digital engagement

- Reduced customer churn

- Expanded financial product adoption

That value justifies institutional payments to Zelle, reinforcing the network’s revenue model.

How Does Zelle Make Money? Core Revenue Streams Explained

Let’s break down Zelle’s monetization structure in practical terms that founders can apply.

1. Institutional Transaction Fees

Banks pay small fees for payment processing and infrastructure access.

2. Payment Infrastructure Licensing

Revenue comes from:

- API integrations

- Payment routing

- Transaction authentication

3. Fraud Detection & Risk Technology

Security is a revenue driver, not just a compliance requirement.

4. Ecosystem Growth Value

Indirect revenue includes:

- Banking engagement improvements

- Digital retention metrics

- Customer lifecycle expansion

Expert Insight:

“The most successful fintech platforms monetize infrastructure rather than end users.”

How Does Zelle Leverage Security and Trust to Make Money?

Security is the hidden engine driving Zelle’s rapid growth, ensuring users can send and receive money with complete confidence.

Key trust features include bank-level encryption to protect sensitive data, account verification to confirm identities, behavioral fraud monitoring to detect unusual activity, and real-time risk scoring to prevent threats before they impact transactions.

Together, these measures create a seamless and secure payment experience that users can rely on every time. As per AppVerticals insights, fintech apps that invest early in fraud detection achieve:

- Higher investor confidence

- Faster institutional partnerships

- Better long-term monetization potential

How Do Zelle Merchant Processing Fees Compare To Venmo or Cash App

Zelle typically has no processing fee for business (merchant) payments, while Venmo and Cash App charge around 2–3% per transaction for business use.

Core Fee Comparison

- Zelle business/merchant payments: 0% processing fee in most cases; Zelle itself does not charge businesses for receiving payments, though a few banks may add their own charges.

- Venmo business profiles: About 1.9% + 0.10 dollars per transaction on payments received by a business profile.

- Cash App for business: Around a 2.75% flat fee on business‑designated payments, with no extra per‑transaction fixed charge.

In practical terms, if a customer pays a business 100 dollars:

Zelle

- Business receives $100 (0% fee)

Venmo Business

- Business receives ~$98.00 (1.9% + $0.10 fee)

Cash App Business

- Business receives $97.25 (2.75% fee)

Feature Trade‑Offs Behind Those Fees

Zelle’s 0% fee comes with fewer merchant tools: no card payments, no integrated checkout, limited invoicing, and no formal dispute framework, so it fits best for trusted, relationship‑based payments (e.g., rent, consulting, B2B).

Venmo and Cash App charge higher merchant fees but provide more consumer‑friendly flows (QR codes, app‑based discovery, basic dispute processes) and better support for casual or retail‑style sales.

Quick Comparison Table

| Aspect | Zelle (Business Use) | Venmo Business Profile | Cash App for Business |

|---|---|---|---|

| Typical processing fee | 0% (bank may vary) | 1.9% + $0.10 per transaction | 2.75% flat per transaction |

| Where money lands | Direct to bank account | Venmo balance, then transfer to bank | Cash App balance, then transfer |

| Card payments | Not supported | Via app and QR, no 3% card fee to buyer for biz payments | Via app and QR/$Cashtag |

| Disputes/chargebacks | Essentially none; payments final | Basic in‑app mediation | Basic refund flow |

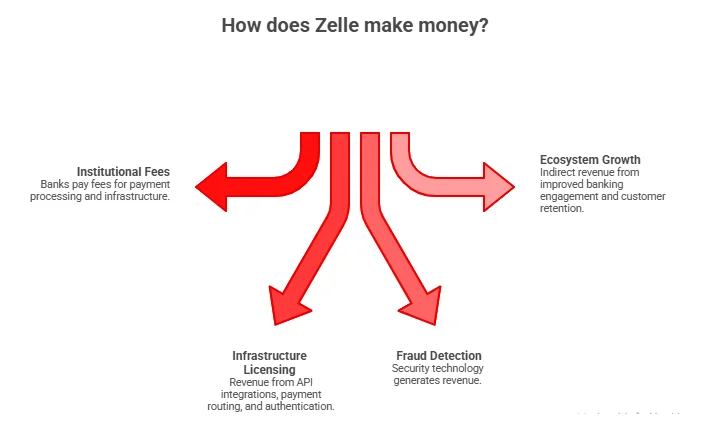

What Is the Major Role of Zelle in the Digital Payment Ecosystem?

Rather than competing with banks, Zelle strengthens their digital transformation efforts. This strategic positioning is a major reason it scales without massive marketing spend. Zelle’s ecosystem role is distinct:

- Instant bank-to-bank payments

- Digital replacement for checks

- Embedded financial infrastructure

What Are the Primary Functions of the Zelle App?

Zelle’s primary function is fast, bank-to-bank digital payments, allowing users to send and receive money directly from their existing bank accounts with built-in security and minimal friction, without needing a separate wallet or balance.

Instant Transfers

Users send funds directly between bank accounts in minutes, a technically complex feature involving real-time payment rails.

Seamless Integration with Banks

Unlike standalone digital wallets, Zelle eliminates extra steps that often slow down adoption. It doesn’t require a separate funding account, comes with built-in identity verification, and significantly reduces onboarding friction, making it easier and faster for users to start sending and receiving money directly from their existing bank accounts.

Security Features

Core features founders must consider:

- Name verification before transfers

- Multi-factor authentication

- Fraud alerts

- Scam detection algorithms

What Must-Have Fintech App Features Should Founders Learn from Zelle?

Through years of building and scaling fintech products as part of our mobile app development projects at AppVerticals, these have become non-negotiable:

Core Platform Features

- Real-time payment engine

- Instant settlement architecture

- Bank API integrations

- Contact-based payments

- Transaction history analytics

Compliance & Security Features

- KYC identity verification

- AML monitoring

- Fraud detection systems

- Encryption and tokenization

- Secure authentication

Growth & Retention Features

- Payment reminders

- Business payment capabilities

- Behavioral analytics

- Automated onboarding

How AppVerticals Helps Founders Build Apps Like Zelle (And Monetize Them Strategically)?

At AppVerticals, we help founders turn fintech ideas into secure, revenue-generating platforms by combining strategic consulting, engineering expertise, and real-world fintech execution experience.

Expert Strategy & Consultation

AppVerticals helps founders:

- Validate fintech product-market fit

- Avoid over-engineered MVPs

- Build monetization models aligned with growth

Payment Infrastructure Integration

We implement:

- Real-time payment rails

- ACH systems

- Secure banking APIs

Security & Compliance Engineering

Our fintech platforms include:

- PCI DSS compliance

- Fraud analytics engines

- AML and regulatory workflows

Scalable Architecture

We design:

- Microservices-based systems

- Cloud-native infrastructure

- API-first platforms

Our experience building fintech products, including rebuilding failing apps, gives founders practical, battle-tested insights.

Key Lessons for Founders, CTOs & Investors

Early focus on network effects, substantial investment in fraud prevention, and optimizing for institutional partnerships further strengthen growth and adoption, creating a resilient and scalable financial platform.

Conclusion: The Real Answer to “How Does Zelle Make Money?”

When founders ask how does Zelle make money, they’re really asking how to build a fintech platform that scales without relying on user fees. Zelle’s success comes from:

- Institutional revenue streams

- Banking partnerships

- Scalable infrastructure

- Security-driven trust

- Embedded finance architecture

At AppVerticals, we help founders apply these lessons to build fintech products that are technically sound, investor-ready, and designed for long-term growth. Understanding Zelle’s model isn’t just about revenue; it’s about building fintech ecosystems that scale with trust and strategic infrastructure.